Rebuild Your credit score Using a Credit Card

Table of Contents

To rebuild your credit the most important is how responsibly you manage and use your credit. You should never be late to pay your credit card bill. Use the online payment option to manage and set your bill payment automatically. The short answer to your question about how long it takes to rebuild credit is dependent on many things but here we are going to discuss how efficiently you can optimize your debt ratio with some already proven tricks.

Optimize your debt ratio – do it without really having to change your spending behavior

Now we get to the fun part, where I’ll teach you the magic number credit agencies really want you to carry in debt and why. Your FICO credit score is calculated using the following formula:

35 percent payment history

30 percent amount owed

15 percent length of history

10 percent new credit

10 percent types of credit

This means the bulk of your credit score is made up of on-time payments and how much available credit you have. Obviously paying your bills on time will improve your credit history over time, so we’ll focus on the debt-to-credit ratio. You should follow the below step strictly to optimize your debt ratio in a meaningful way.

Maintaining low balances on credit cards can raise your score – Credit hack

To optimize your debt ratio, Many experts will tell you to stick to 30 percent of your available credit. This means if you have $1000 of credit, you should only have balances totaling $300.The truth is the more available credit you have, the better your score will be. Maintaining low balances on credit cards can raise your score by up to 100 points. I recommend keeping your available credit at 94 percent. So does Experian.

I checked my own credit report one day and that’s the advice they gave me to raise my own credit score. You should only be spending $6 for every $100 of available credit you have to successfully raise your credit to the best possible score. What this shows creditors is that if something bad happens in your life (medical emergency, job loss, etc.), you still have access to funds to pay your bills for the next six months.

This lowers your credit risk and makes you someone lenders love to work with. So in practice, your credit limit will be five to six times high than your usage limit to game the system. I have another game-changing trick up my sleeves to boost your credit score.

Tricks to increase credit limit quickly – Powerful Lifehack

To optimize your debt ratio you start spending six percent but the problem is only spending six percent of your available credit makes it difficult to gain credit increases from your credit card companies. They’re not going to raise your limits on a card you never use. So, I use this powerful life hack to boost my credit score into the stratosphere, and you can have massive success with it too! What I do is charge and maintain a high balance on each card for two months. In the third month, I pay it all off and let it sit for two months.

This way, I’m using my credit card enough for the bank to continue raising my limit (thus raising my available credit) while maintaining enough available credit to keep the credit agencies happy. Master this method, and you’ll notice your score go within months. And there are a few more insider loopholes to instantly transform your life. All these tricks have the tremendous potential to increase your credit score that is already been proven.

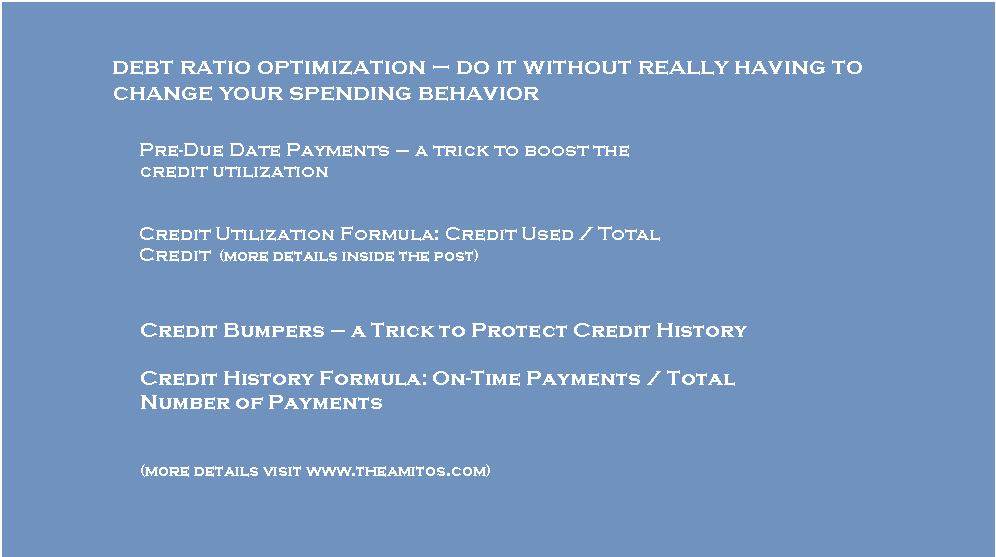

Pre-Due Date Payments – a trick to boost the credit utilization

One trick to boost the credit utilization piece of your score without really having to change your spending behavior is to pay your bill approximately 10 days before your due date.

Example:

Balance: $65

Monthly Spend: $500

Credit Limit: $1065

Due: 25th of each month

Monthly Spend Paid On Due Date (25th of the month): 53% Utilization

Monthly Spend Paid 10 Days Pre-Due Date (15th of the month): 6% Utilization

Credit Utilization Formula: Credit Used / Total Credit

Credit Bumpers – a Trick to Protect Credit History

Just one late payment that happened years ago, maybe when you were back in college, could significantly impact your score today. One trick to absorb some of the impacts of a negative on your Credit History is to use Credit Bumpers by adding more Accounts to your total number of Open Accounts. This example shows how much faster you recover from one late payment when you have 5 open accounts instead of just one.

Example:

1 Account with 1 Missed Payment:

Year 1: 11 On-Time / 12 Total = 91.67% Very Poor

Year 2: 23 On-Time / 24 Total = 95.83% Very Poor

Year 3: 35 On-Time / 36 Total = 97.22% Poor

Year 4: 47 On-Time / 48 Total = 97.92% Poor

Year 5: 59 On-Time / 60 Total = 98.33% Fair

5 Accounts with 1 Missed Payment:

Year 1: 59 On-Time / 60 Total = 98.33% Fair

Year 2: 119 On-Time / 120 Total = 99.17% Good

Year 3: 179 On-Time / 180 Total = 99.44% Good

Year 4: 239 On-Time / 240 Total = 99.58% Excellent

Year 5: 299 On-Time / 300 Total = 99.67% Excellent

Credit History Formula: On-Time Payments / Total Number of Payments

Continue to the next Article (Lifehack to boost credit score – Game the System)

0 Comments